by angelina | Mar 16, 2020 | Advisors, Blog, employee benefits, Estate Planning, Families, Family, Family Market, health benefits, Individuals, investment, Investments, life insurance, Mortgage, tax

[av_one_full first min_height=” vertical_alignment=” space=” custom_margin=” margin=’0px’ padding=’0px’ border=” border_color=” radius=’0px’ background_color=” src=”...

by angelina | Mar 9, 2020 | Advisors, Blog, employee benefits, Estate Planning, Families, Family, Family Market, health benefits, Individuals, investment, Investments, life insurance, Mortgage, tax

[av_image src=’https://financialtechtools.ca/wp-content/uploads/2020/03/insurancePlanningforBusinessOwnersFTT-1.jpg’ attachment=’7681′ attachment_size=’full’ align=’center’ styling=” hover=” link=”...

by angelina | Mar 3, 2020 | Advisors, Blog, employee benefits, Estate Planning, Families, Family, Family Market, health benefits, Individuals, investment, Investments, life insurance, Mortgage, tax

[av_one_full first min_height=” vertical_alignment=” space=” custom_margin=” margin=’0px’ padding=’0px’ border=” border_color=” radius=’0px’ background_color=” src=”...

by angelina | Mar 2, 2020 | Advisors, Blog, employee benefits, Estate Planning, Families, Family, Family Market, health benefits, Individuals, investment, Investments, life insurance, Mortgage, tax

[av_one_full first min_height=” vertical_alignment=” space=” custom_margin=” margin=’0px’ padding=’0px’ border=” border_color=” radius=’0px’ background_color=” src=”...

by angelina | Feb 24, 2020 | Advisors, Blog, employee benefits, Estate Planning, Families, Family, Family Market, health benefits, Individuals, investment, Investments, life insurance, Mortgage, tax

[av_image src=’https://financialtechtools.ca/wp-content/uploads/2020/02/insurancePlanningYoungFamiliesFTT.jpeg’ attachment=’7634′ attachment_size=’full’ align=’center’ styling=” hover=” link=”...

by angelina | Feb 21, 2020 | Advisors, Blog, employee benefits, Estate Planning, Families, Family, Family Market, health benefits, Individuals, investment, Investments, life insurance, Mortgage, tax

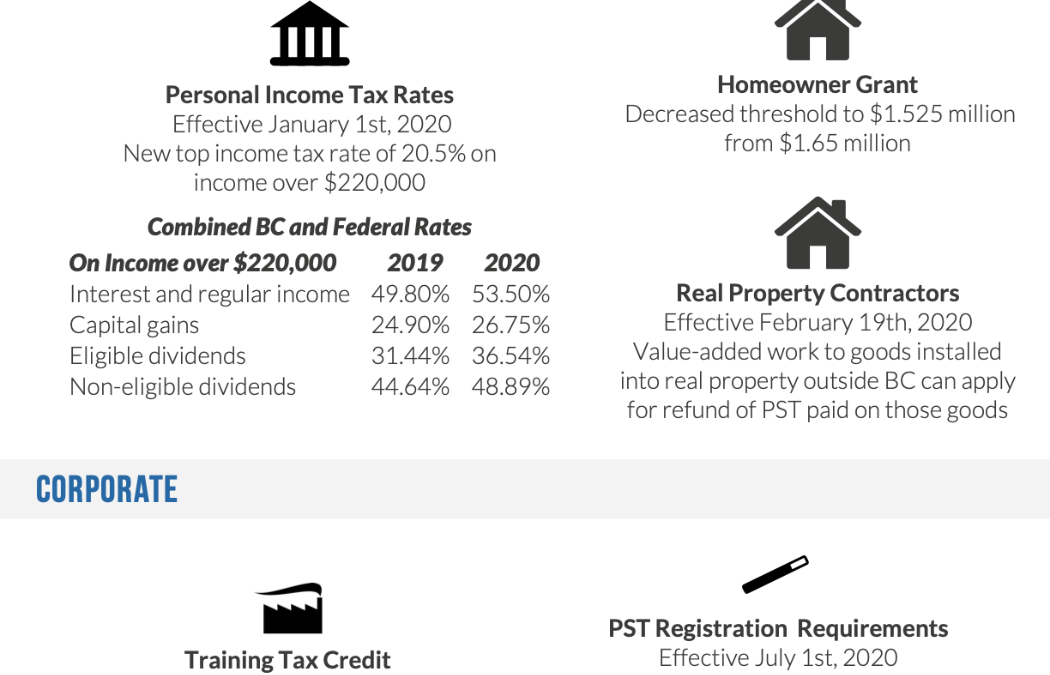

[av_image src=’https://financialtechtools.ca/wp-content/uploads/2020/02/Angelina_Hung_BC_Budget_2020_revised_infographic.png’ attachment=’7626′ attachment_size=’full’ align=’center’ styling=” hover=”...